Many of our members have raised inquiries about VAT on invoices, and we'd like to guide you on its appropriate usage. We've encountered some scenarios where the addition of VAT to an invoice led to a payment dispute between members.

VAT charge eligibility

Businesses operating on the Exchange with a taxable turnover of more than £85,000 must register for VAT. Members below this threshold can, however, also be registered for VAT.

Members can only charge VAT once they've received their VAT number, and the Exchange has verified this. Once they've successfully been registered, they are eligible to charge VAT on their invoices in addition to their base rate for services.

For more on VAT eligibility, visit GOV.UK.

How to check if a member is VAT registered

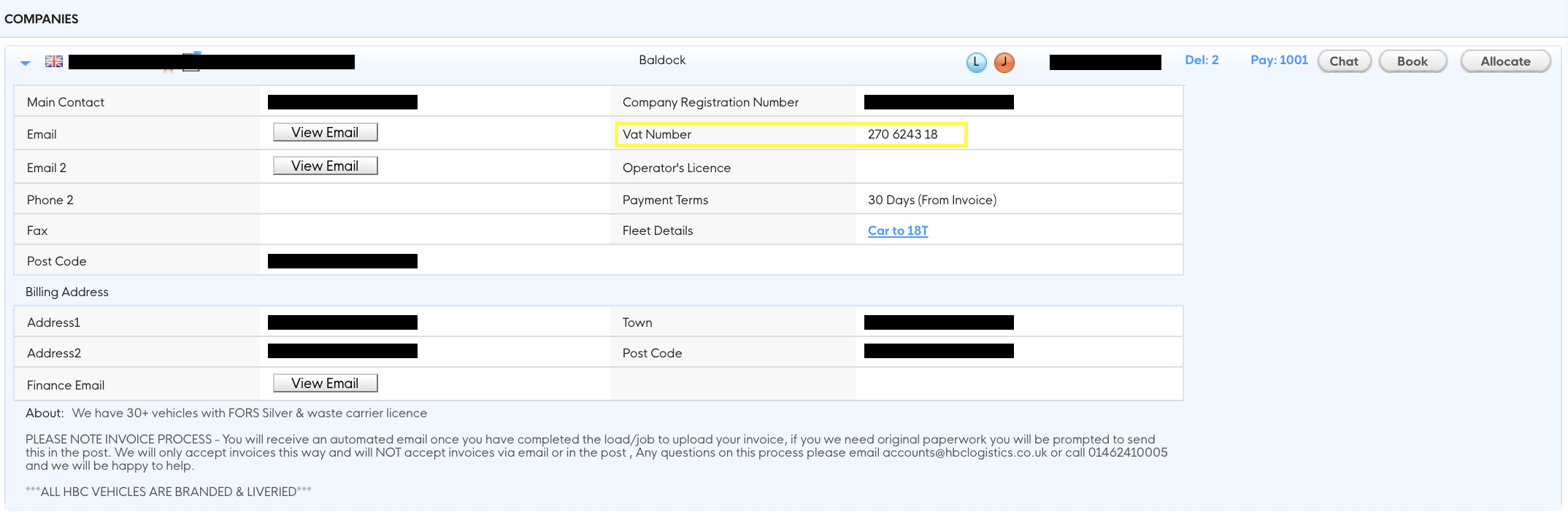

If you see VAT on an invoice and would like to confirm that the other member is VAT registered, you can find that information in their company profile on the Exchange.

Types of VAT charges on the Exchange

There are two types of VAT charged by members on the Exchange. The standard 20% VAT or the 10% Flat Rate scheme.

VAT charges by registered members are necessary and cannot go unpaid regardless of whether the invoice's payer is VAT registered.

Quotes

All quotes submitted on the Exchange are excluding VAT. The VAT charge is added to the invoice when created with the total gross amount due. Any instructions from the load poster about VAT payment in the load notes will be disregarded upon receipt of the invoice.

VAT regulations on the Exchange

VAT cannot be applied to invoices unless our Exchange team has verified a VAT number. Any member on the Exchange using VAT unlawfully could face prosecution by HMRC.

We strongly recommend all members posting more than 20 loads per month be VAT registered. This is for your own protection and peace of mind. Becoming VAT registered means you can reclaim VAT where appropriate and grow your business without worrying about crossing the VAT threshold and being penalised by HMRC. As with any important business decision, we recommend that you consult with your accountant and take advice where appropriate.

Please use the following guide to know whether you need to charge VAT:

Note: We define Load Takers as members quoting on loads, and Load Posters as members posting loads to the Exchange.

- A UK VAT registered Load Taker completes a load with a UK start and a UK endpoint for a Load Poster. The Load Taker will charge VAT.

- A UK VAT registered Load Taker completes a load from the EU/outside the UK to a UK location for a Load Poster. The Load Taker will not charge VAT.

- The UK VAT registered Load Taker completes a load from the UK to a location in the EU/outside the UK for a Load Poster. The Load Taker will not charge VAT.

- When a UK VAT registered Load Taker completes a UK leg of a journey for a load entering the UK or leaving the UK. The Load Taker will not charge VAT.

In all of the above cases, it does not matter whether the load poster is UK or non-UK based. However, in the case of doubt or if you have further questions, please contact your accountant.

For information on this topic please click here.